ViniyogIndia Momentum Portfolio invests in a basket of strongly trending Stocks & ETFs. This portfolio is suitable for Aggressive investors.

ViniyogIndia offers model portfolios based on Quantitative Factor-based strategies. Factors are quantitative attributes that can be used to explain asset returns.

Mathematically, if we try to model Asset Pricing behavior as a liner multivariate function, then factors represent the independent or explanatory variables of the function.

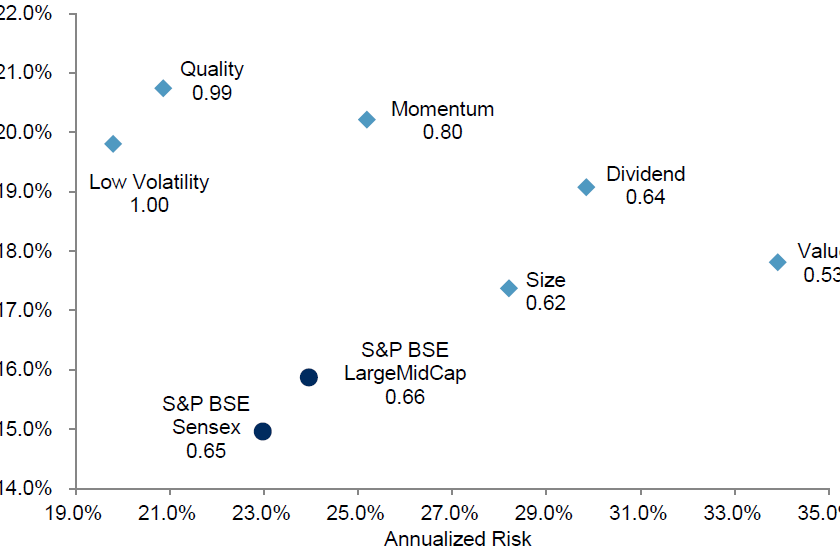

Factor strategies have been extensively researched globally as well as in India. The below chart for example, summarizes the risk-return characteristics of single-factor portfolios in India between October 2005 and June 2017. Over the period, all major single-factor portfolios outperformed the S&P LargeMidCap.

ViniyogIndia’s factor portfolios use a combination of factors that are proven to work well in the Indian markets.

Source: S&P Dow Jones Indices LLC. Data from October 2005 to June 2017. Index performance based on total return in INR. Past performance is no guarantee of future results

Portfolio Design Rules

The basic idea behind momentum investing is intuitive. A stock or any other asset, that has been trending strongly for a while is likely to continue doing so a little while longer. That is the core concept, rest are details.

Nobel Laurette economist Eugene Fama, who propounded the Efficient Market Hypothesis (EMH), described momentum as a “premier anomaly” and termed it a “pervasive” phenomenon. It has been found to work across markets and asset class. Momentum investing remains an extensively researched subject in finance with papers documenting evidence of momentum in stock prices dating almost a century back.

ViniyogIndia Momentum Portfolio applies momentum investing strategy to the Indian markets.

- Portfolio of top ~20 stocks picked from NSE universe demonstrating strong uptrend.

- Further refined using secondary factor(s) to optimize risk-adjusted returns

- Illiquidity filter to remove low volume/ turnover stocks

- Balanced quarterly in order to keep transaction costs low.

Risk Management Rules

Limits on exposure to any single stock or sector

Suitability

This portfolio is suitable for aggressive investors.

Performance measurement & attribution

To interpret the sources of return for our strategy we perform a regression analysis using Carhart 4 Factor Model. The results are shown in the table below:

| Alpha | MKT | SMB | HML | WML | |

|---|---|---|---|---|---|

| Factor exposure | 0.856 | 0.656 | 0.107 | 0.145 | 0.394 |

| p-value | 0.003 | ~0.0 | 0.11 | 0.018 | ~0.0 |

Monthly alpha or excess return for the strategy is 0.856%. This is generated using a combination of secondary factors and asset allocation strategies that tries to enhance momentum returns while reducing risks.

Additionally, standard factors, such market beta, value, etc. also add to the overall strategy returns. Returns from the size factor isn’t statistically significant.

Subscribe to this portfolio monthly @ 0.15% of assets

Investments in securities markets are subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, membership of BASL and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.