The other day, I saw a question on Quora asking how to be a millionaire in India, without investing tons. Needless to say, the requester had meant 1M USD & not INR. All sorts of amusing responses were posted, starting from day trading to FNO and what not. Unfortunately, these are all excellent ways to lose your capital very fast; forget becoming a millionaire.

Becoming a millionaire however may not be as illusionary as it seems. In fact, you can potentially become a dollar millionaire by investing as little as Rs 1500 (or 21 USD) a month. Further, your total capital requirement could be just over 7 Lakhs or 10K USD, which is roughly 1% of your final portfolio size of 7 crores, or 1M USD.

What is the catch?

The only catch is, you need to invest 1516 INR every month continuously for an extended period. Rest is all thanks to compounding, or the ‘eighth wonder’ as Einstein would have it!

Sounds, too good to be true? Let’s figure out this works.

Fig. 1 Building a million dollar portfolio may not be as illusionary as it seems

Between 1981 and 2017, Sensex (excluding dividends) grew at a rate of 16.2% compounded. Rs 1 Lakh invested in Sensex in 1981 is worth around 2.59 crores today (2017) without considering dividends. Assuming 0.5% dividend, total value of the investment would be worth more than 3 crores today.

If we extrapolate this 16.2% return over the next 40 years, a 25 year old Indian can invest 1516 INR on the index each month and potentially generate a retirement corpus of 7 Crores (1M USD) by the time he reaches at 65. Total capital invested over 40 years period would be 7.28L INR or 10.4K USD.

Monthly contribution = FVxR/[(1+R)^n-1]

Where:

FV = Future Value [7 crores],

R = interest rate per month [16.2%/12], and

n = number of monthly installments [12×40].

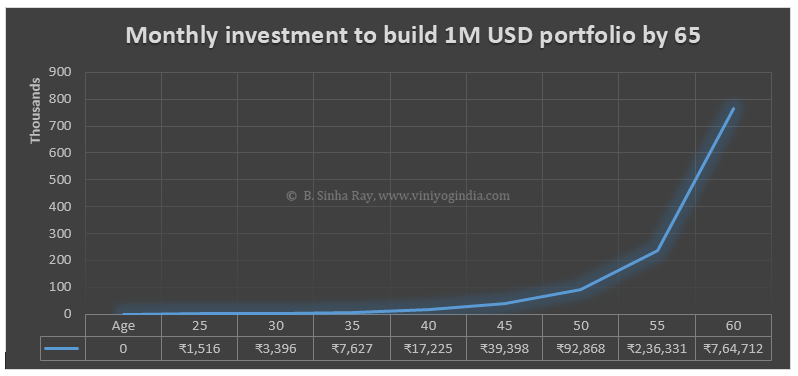

Monthly contribution however increases from a paltry 1516 INR when starting age 25 years to as high as 2,36,331 at 55 years – more than 155 times the initial value. This is why it is essential to start investing early. Time is the lever that makes compounding so magical.

Fig. 2 Monthly investment to build a million dollar portfolio at 65, by starting age

Of course our hypothesis is based on the assumption that past performance can be extrapolated over next 40 years, which is usually not the case. In addition… while we haven’t considered dividends when measuring past performance, we also haven’t provisioned for LTCG which wasn’t applicable in past, but stands at 10% as on date.

However, while it can be argued that broad index returns can potentially reduce going forward, it can also be argued that an investor can improve performance by opting for alternatives such as investing in midcap index or strategy indices. Some of these indices have generally provided better returns than Sensex or Nifty over long-term.

Table 1. Mid & Smallcap indices have beaten the broader indices over past 14 years

The other interesting aspect of this strategy is how the capital requirement changes with starting age, as we strive to build one million USD portfolio by the time investor turns 65.

Table 2. Capital requirement to build a million dollar portfolio by starting age

Above table and the chart following illustrates this in detail:

Fig 3. Capital requirement to build a million dollar portfolio exponentially rises with age

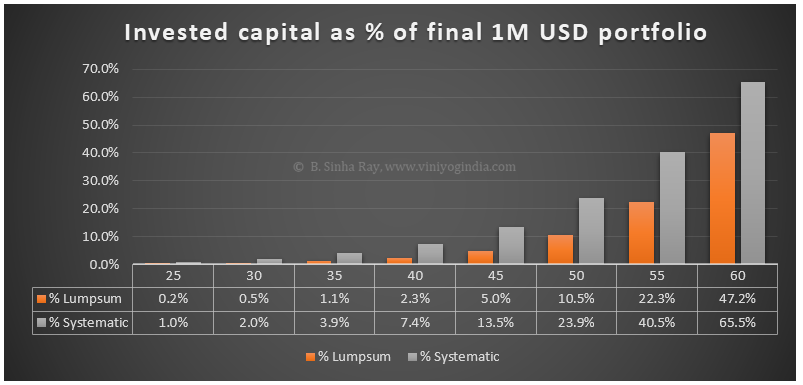

As we saw, it is quite possible to build one million USD portfolio by investing as little as 1500 INR each month (around 21 dollars). Even more surprising, total invested capital could be as little as 1% of the final outcome for systematic investment & 0.2% for lump sum. The only catch is, you need to stay invested continuously for 40 years, and let compounding do its magic.

And if you wish to reduce the wait time, just invest a bit more every month! 250 dollars a month starting 25 could potentially make you millionaire before your 50th birthday!

At the same time, building desired portfolio becomes increasingly difficult as the investment duration shrinks.

So if you want to become wealthy, all you need to do is start early, invest in a reasonable index, and then just wait and enjoy life!

It has come to my attention that unknown persons are fraudulently impersonating me and misusing…

A. Vision and Mission statements for investors Vision Invest with knowledge & safety Mission Every…

**⚠️ IMPORTANT PUBLIC WARNING – INVESTOR ALERT**

Curated portfolio of high performing smallcap stocks. Suitable for aggressive investors.

ViniyogIndia Value portfolio is based on a multifactor strategy that uses Value as its primary…

Adaptive multifactor portfolio of stocks where the factor exposures are dynamically realigned. Suitable for moderately…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}